Search

Search

Learn

Learn

What we’ll cover:

- Prime rates – what are they?

- What prime rates impact.

- How these rate changes affect your mortgage.

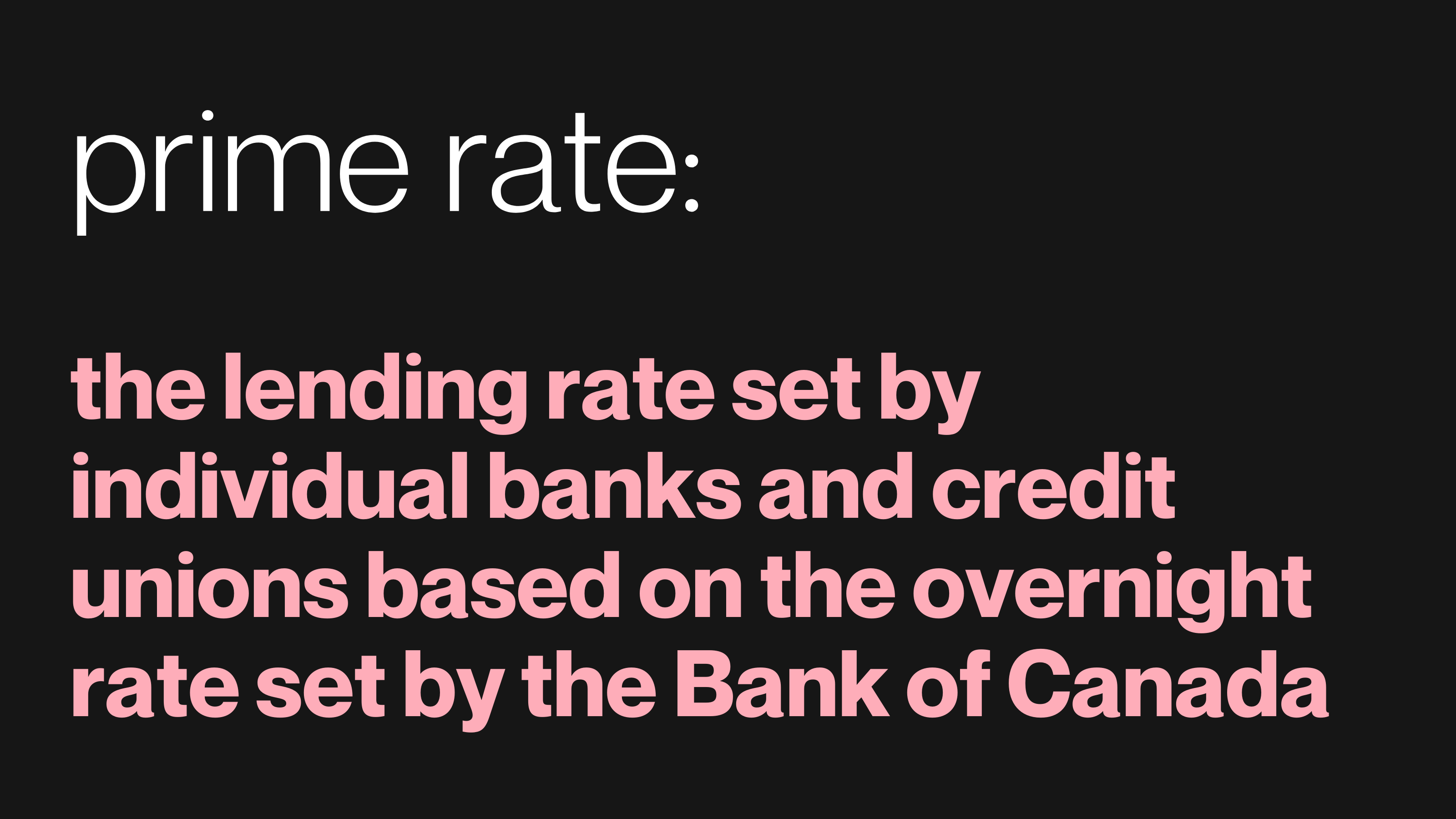

What Is a Prime Rate?

Quick Facts:

- Banks typically have the same prime rate

- Banks adjust their prime rate based on the overnight rate set by the Bank of Canada

- If the BoC (Bank of Canada) changes their rate, banks will adjust theirs by the same amount

The Bank of Canada is our nation’s central bank and its function is to regulate inflation and exchange rates, design and produce our physical currency, and provide fund management for the government. The Bank of Canada will rise and decrease interest rates to support the economy. It raises the target overnight rate in increments called basis points. What is the value of a basis point you ask?

Close, but not quite. A basis point is 1/100th of 1%. If the Bank of Canada raised the prime rate by 50 basis points, that would be 0.5%.

To give you even more context, at the time of writing this, the prime rate is set at 3.70% and the overnight rate is 1.50%. In 2020 the Bank of Canada set its overnight rate to 0.25% at its lowest point, which meant the prime rate was 2.45%.

Why is the prime rate higher than the overnight rate?

Think of it this way: The overnight rate determines the rate at which banks can borrow and lend money. But banks (and credit unions) must account for their own fees and costs behind lending, hence the higher prime rate.

An Increase is Coming…What Does it Affect?

'So, it's very likely that the Bank of Canada will increase rates again on July 13th and what that means is your interest rate will go up as soon as the prime lending rate increases on anything linked to a variable rate. So most commonly those are things like lines of credit, home equity lines of credit, variable rates on mortgages and so on,’ says Sean Hurst, Treasurer at connectFirst.

|

A variable rate means that the interest rate is prime + a set amount by a financial institution or credit union.

The variable part is reflective of the changing overnight and prime rates. In contrast to variable rates are fixed rates, meaning you pay the same amount throughout your loan’s term.

|